After a strong and steady climb for U.S. stocks, they are taking a breather. In 2014, gains for stocks narrowed and in 2015, gains on equities were hard to come by for a majority of investors.

The good news is a long-term bull trend is in play and declines in stocks are a natural, normal part of the investing process. If investing in stocks was easy and there was no risk, there would be no returns.

We were just through 2008, a nice upturn since then and now we face a normal pullback. There are several key ways to help you stay the course in this sort of market environment.

My number one suggestion is to stop listening to hyperbole from the media. Newscasters, pundits, and prognosticators love to make headlines and draw your attention with dire predictions of the end of the world. The world will only end once and this isn’t it. Even 2008, which was the worst year for the S&P 500 since the Great Depression, had a recovery in short order.

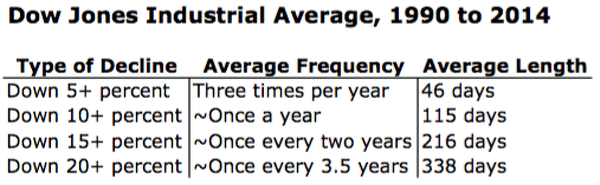

Turn off CNBC and take a look at the facts. According to Capital Group, the Dow Jones Industrial Average from 1900 to 2014 experienced typical declines with smaller percentage downturns coming more often and larger moves were occurring less frequently.

Table courtesy of 2015 American Funds Distributors,

Past results are not predictive of results in future periods

The Dow Jones Industrial Average Index (DJIA) is down 5.87 percent so far in 2015 as of Feb. 4, 2016 but was down much more during January. On Jan. 20, the Dow hit 15,766.74, down almost 10 percent in less than one month.

When investors mention that stocks or equities are long-term investments, it is because in general, the shorter your holding period, the greater your chance of experiencing loss. For instance, if you compare a one year holding period to a ten year holding period for stocks, historically there is a 73 percent chance of a positive return for equities for a one year period but a 95 percent chance of a positive outcome for 10-year holding period.

Looking at it another way, if you hold stocks for one year, these is a 27 percent chance you will lose money. However, if you invest for 10 years, your return is only negative five percent of the time. Always remember — because I have to say it — past performance is no guarantee of future results.

I often tell clients that I can’t guarantee positive results but I can guarantee that some years, they will lose money. Be aware that market downturns and recessions are a natural part of the economy and be prepared for that when investing. If money is needed quickly, having cash available in an emergency savings is a good idea. Typically, six months of expenses is sufficient.

Keep in mind that negative commentary and market lows are made on bad news. Just as strong bull markets end on euphoria, downtrends end on high levels of bearishness. It often pays to buy when everyone is negative and sell when everyone is greedy.

There has been much research on the psychology of investing and studies show that for most people losses feel twice as bad as gains feel good. The reality is that selling means you lock in losses and lose the chance to take part in any recovery. In a long-term bull market, this can be a costly mistake.

If you are investing each paycheck into your employer’s retirement plan or putting money monthly into mutual funds, keep going. The beauty of dollar cost averaging (putting money in on a regular basis) is that the real advantage comes during times when the markets are down. Ever see a really good deal on an outfit or cellphone? It still has the same quality and worth but suddenly it costs 20 percent less. That’s what happens when stocks go down in tandem: good quality stocks sink with the rest so that values emerge. That’s when you make your money investing.

If it is difficult to stay the course, advisors are knowledgeable and help investors make the sometimes hard decision to keep money invested or even invest more when it may feel risky. The reality is that the markets carry more risk when they are high and overvalued.